Explore the results of MFS' annual retirement survey

This article was provided by MFS Investment Management.

In this retirement insight, we share the responses from Canadian members in three sections: market event impacts, retirement confidence and the power of quality advice.

1. Market events are impacting member psyche

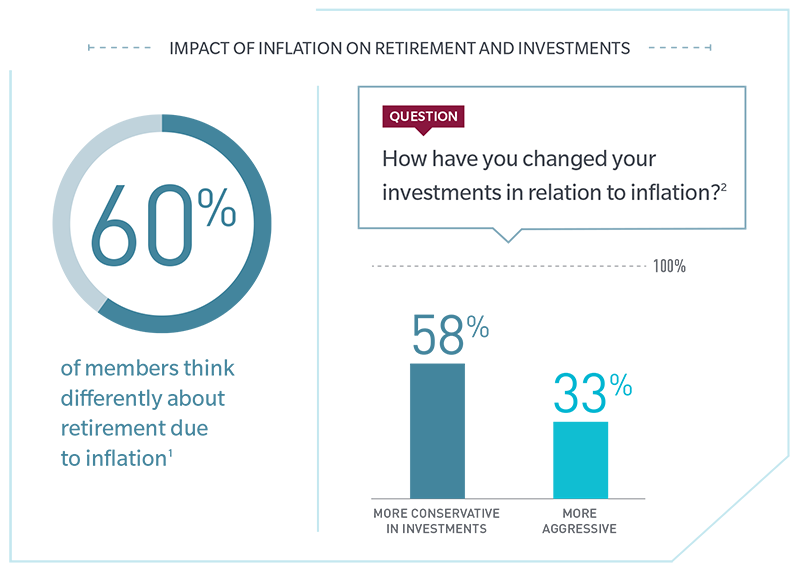

Events of the past three years have members on edge. One concern is, record levels of inflation have compounded their anxiety, causing members to think differently about retirement. Results were consistent across men and women: slightly lower for men at 58% and moderately higher for women at 62%.

In addition to the impact of inflation, the retirement crisis continues to loom. Members also feel they will need to save more than planned (70%) and work longer than planned (54%) due to the current environment.2

“The opportunity for plan sponsors and advisors is to use this moment to educate workers on the features and potential benefits of staying invested, as well as how to get back on track and stay on track towards achieving their retirement goals,” said Jeri Savage, MFS Investment Management’s retirement lead strategist.

1Q: The recent increase in inflation has not caused me to think differently about retirement or my retirement savings. Percentage represents the sum of respondents who strongly disagree, somewhat disagree, or neither agree nor disagree with the statement.

2Q: Please indicate how strongly you agree or disagree with each statement about how the current inflationary environment will affect your retirement and retirement saving.

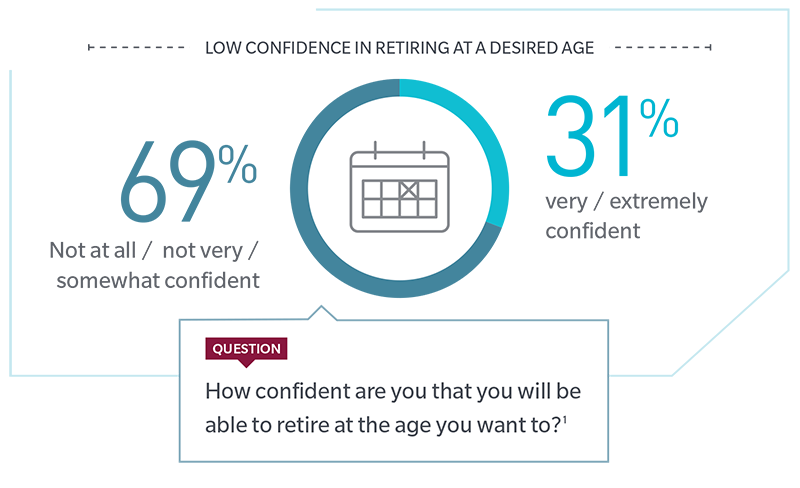

2. Increasing anxiety can manifest in lower retirement confidence

Given member anxiety levels are up since our 2022 survey, it’s not surprising that retirement confidence is low. More members think they may not be able to retire at all, which may have an impact on the workforce.

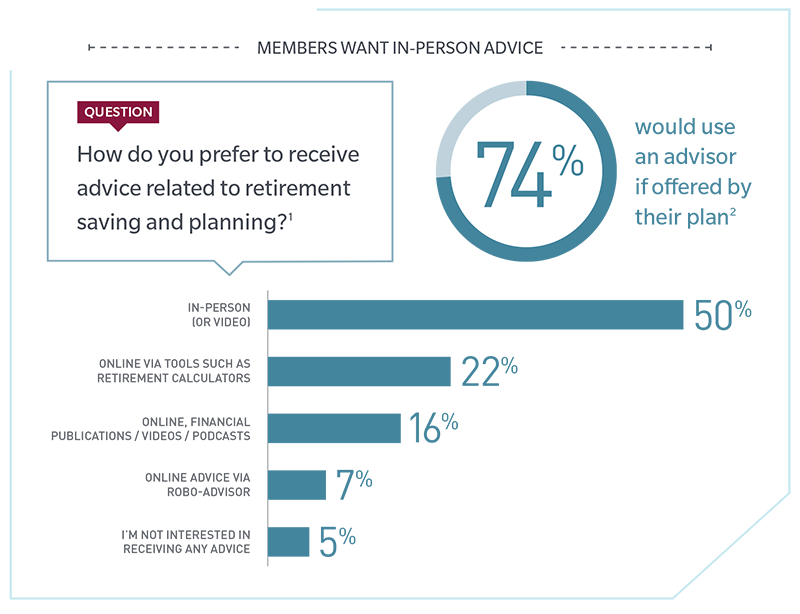

1Q: How do you prefer to receive advice related to retirement saving and planning? “In-person” can be a video call.

2Q: If your workplace retirement plan offered access to an advisor/planner to help with planning for retirement, would you use this resource?

3. The power of advice

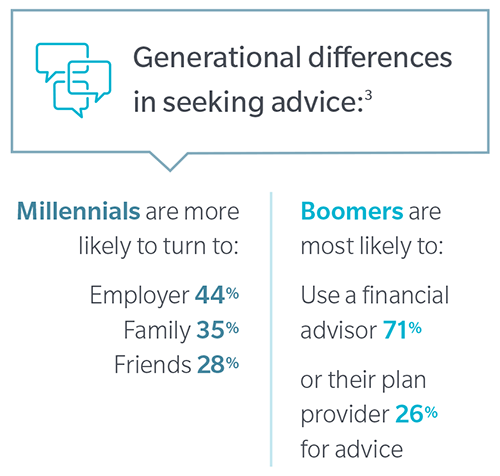

Some drivers of retirement confidence, such as bear markets or inflation, are beyond control. However, access to quality advice is not, and it can be a powerful tool to boost retirement confidence. Members indicate a preference in speaking with a financial advisor when it comes to advice. Trusted and personalized advice can be one of the most valuable tools for plan members.

When it comes to retirement advice, members use a variety of sources, from advisors to family members to online services.3 Recognizing these preferences is important, and plan sponsors can satisfy them by providing access to multiple sources of advice.

1Q: How do you prefer to receive advice related to retirement saving and planning? “In-person” can be a video call.

2Q: If your workplace retirement plan offered access to an advisor/planner to help with planning for retirement, would you use this resource?

3Q: What resources do you use to help make investment and/or retirement planning decisions?

Actions to consider taking

While solving the crisis will take our combined efforts, there are some actions that plan sponsors can take.

“Each participant is unique based on their financial needs, goals and risk tolerance, and a wide array of solutions will be needed to address varying participant needs.”

- Jeri Savage, Retirement Lead Strategist,

MFS Investment Management

Market Events: Members often look for information or advice during market volatility. Plan sponsors and advisors can use this as an opportunity to educate them on the features and potential benefits of staying invested.

This includes communicating with those near retirement as well as much younger plan members. Consider if your plan has the tools and resources available to help members stay on track.

Retirement Confidence: Members expect a more gradual transition into retirement, possibly reducing hours or switching jobs. The traditional view of retirement may no longer resonate with many employees.

Why should we care about this sentiment around a gradual transition into retirement rather than a hard stop?

It could have implications for workforce management. For example, policies that allow employees to gradually wind down before retirement, might offer opportunity for a better transition for both the retiree and the new person filling that role. Explore how employees retire. Would a gradual transition support healthy workforce turnover?

Power of Advice: While members use a variety of resources for advice, plan sponsors are a natural hub from which members can access to receive advice, education and tools.

Consider offering access to a comprehensive financial wellness program that can support plan members in planning for retirement.

For more details, plan sponsors may reach out to your MFS representative.

Survey Methodology

Source: 2023 MFS Global Retirement Survey, Canadian Results.

Methodology: Dynata, an independent third-party research provider, conducted a study among 1,004 Defined Contribution (DC) plan members in Canada on behalf of MFS. MFS was not identified as the sponsor of the study.

To qualify for the survey, DC plan members had to be over 18 years of age, employed at least part-time, and actively contributing to a DC Pension Plan, Group Registered Retirement Savings Plan, Deferred Profit Sharing Plan, NonRegistered Group Savings Plan, or Simplified Employee Pension Plan. Data weighted to mirror the age gender distribution of the workforce. The survey was fielded between March 22 and April 6, 2023.

Generational cohorts have been defined as follows: Millennial ages 26–41; Generation X ages 42–57; Baby Boomer ages 58–77.

Issued in Canada by MFS Investment Management Canada Limited.

The views expressed in this material are those of the presenter. For informational purposes only. These views should not be relied upon as investment advice, as securities recommendations, or as an indication of trading intent on behalf of any MFS investment product.

Please check with your firm's Compliance Department before initiating events to verify that the activity complies with your firm’s policy and industry rules. MFS does not provide legal, tax or accounting advice.

58204.1