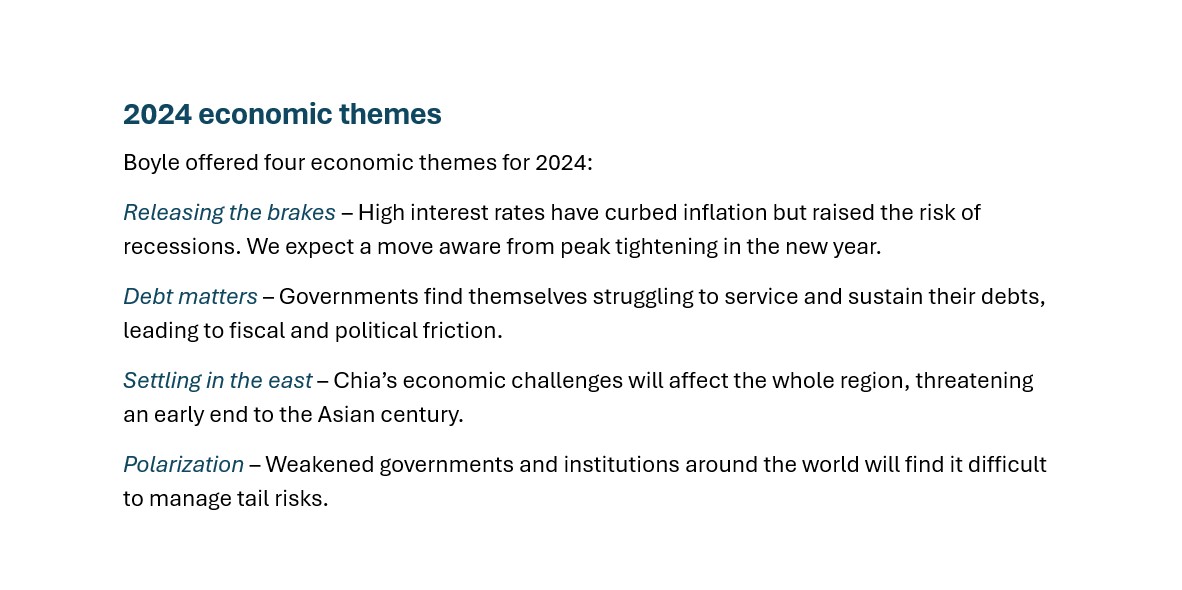

Northern Trust's Ryan James Boyle says we survived 2023, now we can survive 2024

2023 was a great year despite some of the challenges we faced, says Ryan James Boyle, senior vice-president and senior economist at Northern Trust. Speaking at CPBI's Economic Outlook conference in the keynote session, Sticking the Soft Landing, he said we managed to get through the war in Ukraine and the Middle East and a volatile economy, “and we’re still here. We got through a lot, but we got through it.”

Throughout the year, Boyle and his colleagues posted monthly forecasts on Northern Trust’s website. “We never called a recession,” he says. “And a year ago, that was a nervous position. I was defensive and offered all the caveats and things that could go wrong. But it worked out.” That’s why he called his presentation, Sticking the Soft Landing. Despite the continued challenges we will face going into 2024, we will get through it.

Economic activity exceeds expectations

“Activity has exceeded expectations so far this year,” says Boyle. “Consumers, buoyed by strong job markets, have been the main contributor to overperformance. Government spending has also been robust. However, there is moderation ahead because household finances are normalizing with less saving and more borrowing. We’re finding consumer sentiment is coming back. A lot of this is driven by big government inflation. The job market is also showing some signs of cooling.

“Consumer sentiment was terrible. It was at its worst when gasoline prices reached their peak. In hindsight, we were much more upset about expensive gasoline than we were about a potentially fatal respiratory pandemic. But we're finding consumer sentiment is coming back. A lot of this is driven by big government inflation.

“However, actions speak louder than words, and even as we say the economy's bad, consumers are still planning holidays and still spending. That's an important leading indicator. If people fear they will lose their jobs they won’t travel. At the same time, consumers are taking on debt and delinquency rates are trending up.”

Markets moving up timeline of expected rate cuts

As for markets, they have been moving up the timeline of expected rate cuts, says Boyle. Favourable views of the inflation data have caused bond rallies. As well, the first easing of monetary policy is expected, and more cuts are expected in 2024. It’s not a matter of when it starts, but how many we will see. We think it will be a long while before we see the first rate cut.

In addition, “inflation has fallen but remains too high. Russia and Ukraine impacted commodity prices, especially in energy and food. That added to the inflationary cycle that was comfortable worldwide, and central banks responded in a globally consistent manner. Now they're ready to accommodate in a way that looks pretty familiar.”

Volatility was muted in equity markets but rampant for debt instruments in 2023. The repricing during the year was easily explained by the rising rate environment, says Boyle. “Selloffs in 2023 were likely overdone. Investors are seeking interest income and equity risk premium will likely be very low in the coming year.

After a long period of low interest rates, yields had risen sharply around the world. Now central banks have been raising rates and reducing their balance sheets. Government borrowing costs are rising rapidly and debt has increased, especially over the last two years. “Much of it has been funded with short-term instruments,” says Boyle. “With interest costs absorbing increasing amounts of government revenue, this may limit the amount of stimulus that can be applied if a recession arrives.”

China changing global economy

Another key trend as we move into 2024 is that China is entering some structural changes. “The pandemic has accelerated and exacerbated these changes and they are not seeing the foreign direct investment that they have for decades. They're facing competition in a way they haven’t previously,” says Boyle. He says North America needs to reconsider its supply chain, a lesson learned from the pandemic. It doesn’t make sense to source the majority of the world’s semiconductors in China and Taiwan because things can go wrong.

“At one time, it was a rational business decision to procure so much production from China. It was cost effective, and the supply chains worked so well to get goods where they needed to be on time. But it has already changed.

“China grew the way it did by taking out a lot of debt. Then its property sector looked like it was overbuilt as its population stopped growing. This sector is a big source of jobs. We don't worry too much about this as a global risk because most Chinese debt is held domestically. It's a saving culture and they tend to pay and keep their assets local.

“In North America, demographics is a big, long-run worry. People are living longer, healthier lives. While this sounds great, birth rates are down and this puts a lot of demand on our current workers and can create a productivity gap. We need to get the most out of every worker that we have.” Boyle says this is going to be a real challenge because of a new technology called artificial intelligence that can bring out new productive potential.

“ChatGPT is moving into a few spaces. I've heard the example that attorneys can use ChatGPT for contract templates for boilerplate legal language. However, if your attorney is using AI, make sure you are reading every word because, generally, it is just guessing what the appropriate word is. However, investments are happening. And we are seeing some payoff. It is at once exciting and concerning.”

Boyle says that despite the many economic, social, and technological indicators we need to be aware of, he and his firm believe we will have a soft landing and no recession.

“A soft landing has never happened before,” he says. “Ultimately, many of us economists are just historians, we are looking for past examples to forecast what may happen. We've never really pulled it off like this, where we see inflation coming down, and the bank can loosen interest rates as a result. Central banks usually cut rates because of a crisis; there's usually something that forces their hand and they must react. They have to stimulate the economy and do what they can to manage through. Now they can figure out a path to exactly when and how much loosening.”