Erika Toth, of BMO Global Asset Management, explains the industry’s growth, the key areas attracting capital, and the impact of branding and fees

This article was provided by BMO Global Asset Management.

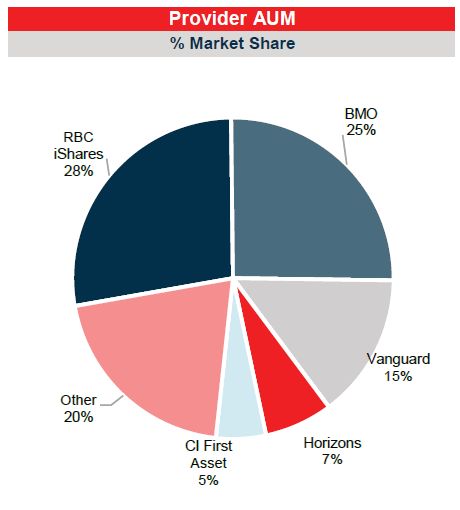

There is no question that the Canadian ETF industry has grown significantly over the last decade, having become popular for their low cost, their transparency, instant diversification, and liquidity benefits. Over the last five years, the industry has doubled in size to C$338 billion in assets under management (AuM). There are now over 1,300 listed products on the Toronto Stock Exchange, offered by 42 different issuers. However, over two-thirds of the industry assets under management (AuM) are managed by the largest three providers (see Chart 1). The 10th Annual 2023 Global ETF Investor Survey, conducted by Brown Brothers Harriman, confirms that issuer brand and experience, management expenses ratios (MERs), and index methodology are at the top of the list of most important criteria when selecting an ETF. In this article, we look at the evolution of ETFs over time, home in on a few key areas attracting interest and capital and consider how the evolution may continue in the future.

Quickly gained popularity

ETFs were first introduced in 1990 in Canada with the launch of the TIPS (Toronto 35 Index Participation Fund) and in the U.S. in 1993 with the launch of the SPDR S&P 500 ETF. Exchange traded funds quickly gained popularity among retail investors, but it wasn’t until the early 2000s that institutional investors, including pension fund managers, began to take notice. One of the first large institutional investors to make a significant allocation to ETFs was the California Public Employees’ Retirement System (CalPERS). In 2000, it invested $1 billion in the SPDR S&P 500 ETF.

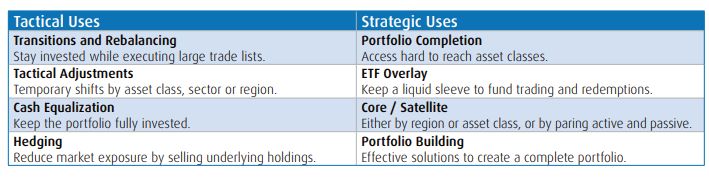

As the number of products and strategies offered grew, they started to appeal to a variety of different user groups including advisors, retail investors, private family offices, asset managers, and institutions like pension funds, endowments, and foundations. Numerous studies and investor surveys over the last decade have confirmed that investors are using ETFs both for longer term strategic allocations and for shorter term tactical uses (see Chart 2 below).

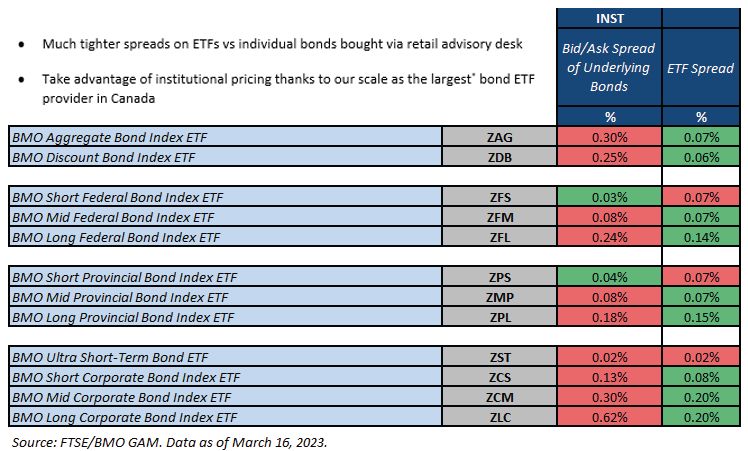

At first, exchange-traded funds were associated with broad equity index exposures. The early 2000s saw the first bond ETFs listed north and south of the border, a tremendous innovation which brought an illiquid, OTC-traded asset class onto the exchange. Institutions are now able to buy a diversified basket of bonds in one trade that targets specific segments of the bond market, credit quality, and duration. Often, the bid-ask spread on the ETF will be tighter than the average spread of the underlying bonds (See Table 1).

Within the fixed income landscape, investors can now pinpoint their desired exposure and allocate to U.S. corporate bonds, ESG-screened corporate bonds, emerging market bonds, or U.S. TIPS for inflation protection, for example. So far in the first quarter of 2023, institutional clients have been allocating to a barbell strategy – allocating to ultra short-term bond and money market ETFs (such as ZST, ZUS.U, and ZMMK) to take advantage of the dramatic rise in interest rates seen over the last year. They have been combining this with long duration government bond exposure (ZFL and ZTL have been two of the top selling fixed income ETFs in Canada so far this year). Using ETFs, a pension fund or asset manager can nimbly lengthen or shorten duration or calibrate the level of credit risk to their desired exposure given market conditions and can do so in a very cost-efficient manner. When bond markets froze up during the onset of the COVID-19 pandemic in March of 2020, many corporate and provincial bonds in Canada went no bid. ETFs were one of the few investment options that remained liquid and many pension fund managers and asset managers used them to quickly adjust their portfolios to reduce risk.

Evolved dramatically

The spectrum of equity ETFs has also evolved dramatically. Smart beta and factor are often referred to as the halfway point between indexing and traditional active management. The investment universe is screened using a specific set of criteria to achieve an investment objective that differs from traditional market capitalization weighting, for example, by reducing risk, or investing in companies with a track record of sustainable dividend growth or profitability. These rules-based strategies are often a fraction of the cost of traditional actively managed mutual funds, yet still offer the potential of outperforming the market. BMO’s Canadian Low Volatility Equity ETF (ZLB, the 2022 recipient of the Lipper Award for Best Fund Over 10 Years in the Canadian Equity Category) has been a popular choice for investors looking for equity exposure with lower drawdown risk in challenging market environments. The quality suite, on the other hand, has resonated with investors looking for companies with a track record of profitability and earnings growth, yet strong balance sheets. Enhanced income strategies, like covered call ETFs, have been popular with investors seeking the tax efficient1 monthly cash flows provided by selling options – be it retail investors or ultra high net worth family offices. As one of the pioneering ETF providers in Canada, many of BMO’s smart beta ETFs now have track records of over 10 years.

Areas of growth for the future

In the last several years, there have been more actively managed, thematic, and alternative investment ETFs launched. It is very likely that these types of strategies will see important growth over the next few years. More asset managers are offering their funds in an ETF wrapper. Most investors, retail and institutional alike, have tended to use active and index strategies simultaneously, in a complementary manner.

Interest in thematic investing has also grown and is sometimes thought of as the next evolution of traditional sector ETFs, focused on areas of the market undergoing rapid innovation such as clean energy, robotics, or artificial intelligence. In recent years, there has been a trend towards socially responsible investing, with environmental, social, and governance (ESG) ETFs experiencing a 40 per cent compound annual growth rate (CAGR) over the last five years, and 43 consecutive months of inflows.2 ESG criteria has become an important consideration for pension fund managers who want to be responsible stewards of capital and invest in companies that align with their values. In Europe, ESG ETFs accounted for 65 per cent of all ETF inflows in 2022.3

In the alternative investment space, infrastructure is an example of how investors have harnessed the benefits of real assets in an exchange-traded vehicle (think: companies that operate toll bridges, wireless towers, and electricity transmission, which have steady cash flows and lower correlations with broad markets). Defined-outcome ETFs would be a natural evolution in the alternatives category.

The ETF industry in Canada has doubled in size over the last five years, and the size of the industry globally indicates that we could be seeing the $500 billion milestone reached over the next three years or so. With market volatility levels reaching extremes in 2008, 2020, and again in 2022, ETFs have not only demonstrated resiliency, but have also proven to be a valuable tool for fund managers looking to tap into liquidity, manage risk, or exploit opportunities.

Erika Toth (CFA) is director, ETF distribution – institutional and advisory, eastern Canada, at BMO Global Asset Management.

- Tax Efficient: as compared to an investment that generates an equivalent amount of interest income

- CEFTA Monthly Report, based on AUM as at February 28, 2023, NEW-CEFTA-February-2023

- The 10th Annual 2023 Global ETF Investor Survey, Brown Brothers Harriman