'You can't have a net-zero portfolio without a net-zero world,' says Aaron White

The world of ESG investing is shedding its labels and facing a reckoning. Once buzzwords, terms like “ESG” and “sustainable investing” are being questioned, if not discarded among institutional investors, in favour of sharper frameworks and more measurable outcomes.

According to industry leaders, that shift is as much about market maturity as it is about political and regulatory backlash.

"Before COVID, it was the intent," said Laila Danechi, senior business development manager at Pictet Asset Management. "Now, the conversation has shifted. It’s no longer about the intent, but about the ‘how’; how managers are imbedding those considerations into their investment process. And it’s the ‘how’ that is the tough nut to crack."

Aaron White, executive director and head of sustainable investments at CIBC Asset Management, agrees, emphasizing that institutional investors. including major pension plans and endowments, are staying the course and even doubling down.

“When you have a much longer investment time horizon, the reality of these risks and opportunities becomes more material,” he said, acknowledging these investors are increasingly aware that meeting long-term objectives, such as net-zero targets, requires contributing to real-world decarbonization.

“You can’t have a net-zero portfolio without a net-zero world,” he added.

For Monika Freyman, VP of sustainable investing at Addenda Capital, ESG has reached a pivotal point where clarity and consistency in terminology are crucial. While terms like ESG, responsible investing, and sustainable investing are often used interchangeably, she prefers “sustainable investing” because it’s broader and more inclusive.

ESG, she explains, refers specifically to environmental, social, and governance factors within investment decisions, while sustainable investing encompasses a whole process - including “being an active owner of your capital” through stewardship and engagement.

White noted that the investment industry has been deliberately distancing itself from the term “ESG,” which he said has become politically charged, and is instead emphasizing the financial relevance of sustainability risks and opportunities. This shift reflects a broader effort by firms to better communicate the tangible value of their sustainability work, particularly in how it contributes to long-term financial performance.

“The industry has really been focused on articulating the value proposition and showcasing to investors and maybe even skeptics the type of work that our teams actually conduct and how they’re interconnected with long-term performance. That’s been critical in terms of us both justifying the importance of sustainability work but also navigating this new environment,” he explained.

Danechi stressed that sustainable investing requires more than simply selecting the right strategy. It also demands a thorough evaluation of the asset management firm behind it. After all, “if they’re not aligned, there is a risk of a disconnect,” she noted.

In fact, she also mentioned that instead of the label “ESG,” she believes it should be “GES,” as everything starts with the “G” for governance.

“Good governance is always key,” she said, underscoring how good governance underpins a company’s ability to manage risk, regardless of sector.

Still, as Danechi is quick to emphasize, “I don’t think ESG is done... Institutional investors are just taking a pause to reassess,” she said.

Credit: Millani

White acknowledged that political volatility - especially in the US - has created uncertainty around ESG, but he sees asset managers responding by sharpening their focus rather than retreating. He emphasized that firms are reinforcing the value of ESG integration by linking it directly to financial performance, adding that the emphasis now is on how research drives better decisions and outcomes.

Closer to home, Danechi pointed to unintended consequences from Canada’s Bill C-59, which aims to combat greenwashing but has prompted firms to remove ESG reports altogether from their website. She believes the lack of consistent, comparable data is making managers pull back, not lean in.

While she doesn’t dispute the importance of oversight, she emphasized the critical effect this bill has had.

“It came from a very good side,” she said, “but actually a lot of investors have scaled back... because it’s very difficult to get the data and comparable data as well.”

White acknowledged that while Canada’s Bill C-59 and related CSA guidance have faced criticism for their lack of clarity - particularly around enforcement and scope - the underlying goal has had a beneficial impact on the industry.

Freyman suggests that Bill C-59 might have been more effective if it had followed the implementation of clear sustainability reporting standards. She argues that introducing the Canadian Sustainability Standards Board (CSSB) guidelines first would have given companies a consistent framework for disclosing climate and ESG-related information.

As a result, investors would have had a standardized framework for reporting material information, she said, adding this, in turn, would have limited the variability and subjectivity in disclosures - preventing the current confusion between “apples and oranges” and reducing reliance on vague or overly polished marketing materials.

“After companies were used to doing good standardized disclosure, it would have been a more natural maturity progression,” she says. “It would have been ideal to bring in the CSSB first.”

Yet, White acknowledged that the ambiguity has forced firms to be far more rigorous in backing up their claims and as a result, “has been very positive for the industry,” he said.

He outlined two key areas where institutional investors are ramping up efforts in response to climate risk. First, he said, there’s a growing emphasis on developing the internal tools, expertise, and frameworks necessary to assess and price climate-related risks across portfolios, noting that asset owners are also placing more scrutiny on how managers are building internal capacity and capabilities in climate science.

Second, he highlighted continued momentum in allocating capital to climate-focused solutions, particularly within private markets, highlighting strong investor demand for infrastructure and decarbonization strategies. He also flagged a rising interest in emerging markets, as well as strategy launches on managing risk in the global south, especially where climate transition intersects with development goals, pointing to opportunities like transitional infrastructure, supporting natural capital solutions, and scaling net-zero aligned industries.

He also observed that in private markets, where asset owners prioritize sustainability, capital is starting to shift accordingly. He explained that investors aiming for net-zero targets are increasingly turning to private equity, credit, and debt because these asset classes offer a more direct path to real-world decarbonization.

“Private markets are primed to actually deliver on that additionality that will drive the transition forward,” said White. “Funds are offering very attractive investment optionality alongside the real-world outcomes.”

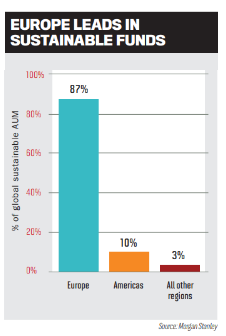

Credit: Morgan Stanley

Looking ahead, Danechi believes the top ESG investment priorities right now are climate transition and biodiversity, but the ways investors approach these issues are evolving. She sees a growing split between two schools of thought in sustainable investing: one focused on “positive impact” - investing only in companies or sectors already aligned with sustainable objectives.

The other is an emerging approach she refers to as "impact improvement" - investing in attractive companies across all sectors, including oil and gas, regardless of their current stage in the transition towards a sustainable, low-carbon economy.

The emphasis is on identifying companies with the potential to enhance and accelerate their transition journey and impact trajectory, particularly through effective engagement and strategic support. This approach emphasizes on selecting firms that are not only well-positioned to transition sustainably but are also likely to benefit from a valuation re-rating in the market, she explained.

According to Danechi, the next big shift will come from this impact improvement mindset as all sectors will need to transition. However, to successfully achieve real impact, structured and well-organized shareholder engagements will be key to driving and accelerating change.

“People aren’t calling it that yet but mark my words, it’s going to be here soon,” she said.