William Blair strategist Olga Bitel on how AI infrastructure, defense spending, and supply-chain investment are expanding opportunities beyond U.S. equities

After a decade defined by narrow, largely intangible businesses driving growth, markets appear to be entering a new phase shaped by physical buildout across AI infrastructure, defense, energy, and supply chains. This shift reflects a broader global building cycle that is driving growth and returns beyond the United States and across a wider range of industries and regions.

A broader market awakening

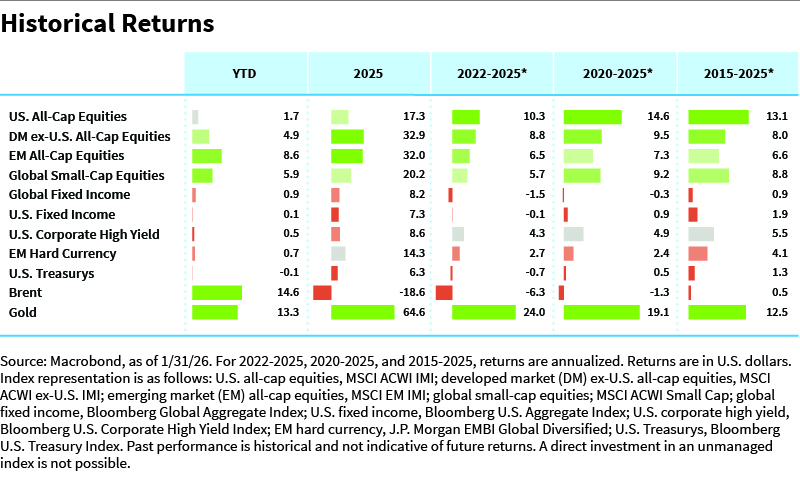

Over the past decade, U.S. equities delivered annualized gains two to four times higher than most alternatives. That is a substantial gap over a long period and it shaped asset-allocation decisions around the world.

Over the past three years, however, that picture has begun to change, with jurisdictions that had been dormant showing signs of life. In 2025, U.S. equities, while still vibrant, lagged both EMs and some developed markets. Early 2026 data show the same pattern.

One change is the industry composition of returns. Leading sectors are asset-heavy industries. Country-level performance shows a similar pattern. Jurisdictions with strong exposure to building and industrial capacity are rising in the rankings.

Two forces driving change

Two forces appear to be acting together to drive this change: technological transformation and geopolitics.

On the technology side, AI has moved from concept to programming to infrastructure buildout. Massive data centers are being built across geographies, and we’ll need to build even more of them as technology becomes a larger portion of everyday life. These facilities will require semiconductors, cooling systems, power infrastructure, and connectivity. They also require roads, airports, transmission lines, and energy supply. This is not confined to one country or region. And the buildout has a long runway.

The second force is geopolitical. Many countries are now pursuing greater economic autonomy. Policymakers are prioritizing national resilience in defense, energy, and supply chains.

Economic autonomy is really about physical growth, so the practical result is increased public and private investment in physical infrastructure and industrial capacity. As governments negotiate trade agreements, fund defense and energy projects, and lower barriers within regional blocs, we’re seeing growth in more places. Canada, Australia, Japan, and much of Europe are moving in this direction at varying speeds.

Building AI capability and building national autonomy now require many of the same inputs. Modern defense is less about legacy hardware and more about drones, remotely operated systems, and software-enabled platforms. Supporting those systems requires critical minerals, electric and magnetic motors, and components that power electrified and autonomous technologies.

Those same inputs extend beyond defense. The infrastructure needed for autonomous logistics, robotics, and advanced manufacturing—such as drones delivering customers’ Amazon and Walmart packages—relies on the same electric and digital backbone.

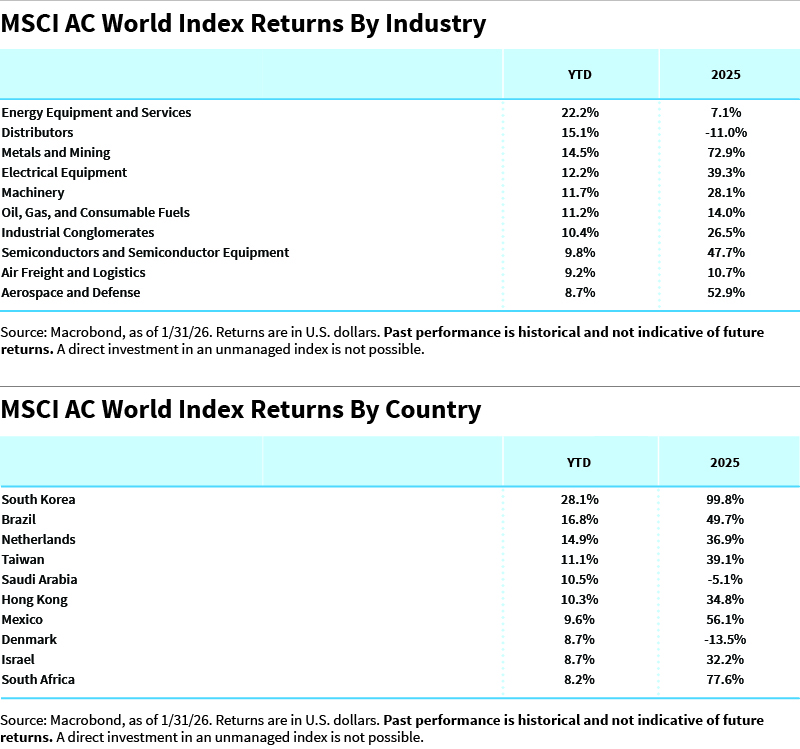

The resulting investment opportunities appear widely dispersed across regions. Defense-related spending is becoming more compelling in places such as Germany and Japan. Technology hardware and semiconductors remain concentrated in established hubs such as Taiwan and South Korea, with Japan also participating. Metals and mining continue to be anchored in many emerging markets, including Mexico, South Africa, and Chile.

Lastly, as growth strengthens and investment accelerates, yield curves typically steepen, creating a more favorable environment for financial institutions. Banks, as the conduit for capital flows, tend to participate broadly in such cycles.

Three questions for investors

Markets are now grappling with several key questions.

The first is the economics of AI infrastructure. Hyperscale technology companies are investing heavily in data centers and related capacity. Will future revenues and profits justify this investment? Or will business models evolve in ways that reduce cash generation? These companies have been central to market performance for years, and the answer will matter for valuations and capital allocation.

The second is the future of software. Demand for software will undoubtedly rise as AI capabilities expand. The question is who will deliver it. Will incumbent providers adapt their existing platforms, or will new entrants capture a meaningful share of the opportunity? Hyperscalers may choose to move further up the stack, embedding applications and workflows into their ecosystems. The allocation of these profit pools remains highly uncertain.

The third is the definition of a “national builder.” As countries pursue economic autonomy, which companies will be allowed to participate in key projects? Will domestic firms be favored, or will suppliers from allied jurisdictions benefit? Legal, financial, and geopolitical considerations will shape access to markets and profits. These decisions will influence which companies capture value from the current investment cycle.

An environment shaped by building

The common thread across these developments is construction—of infrastructure, supply chains, and industrial capacity. Markets are reflecting that shift. Performance leadership is broadening beyond the narrow set of winners that defined the previous decade. The combination of technological investment and geopolitical priorities suggests that this phase may persist. For investors, periods of dislocation often create opportunity. The current environment appears to be one of those periods.

This article is excerpted and edited for length. For more insights, read the full article.

Olga Bitel, partner, is a global strategist at William Blair Investment Management. She is responsible for economic research and analysis across all regions and sectors. Bitel distills macroeconomic and geopolitical developments into actionable insights for global equity portfolios within a multifaceted strategic framework. Before joining William Blair in 2009, Olga was a senior economist at the National Institute of Economic and Social Research in London. Olga received a B.A. from the University of Chicago and an M.Sc. in economics from the London School of Economics and Political Science.

Olga Bitel, partner, is a global strategist at William Blair Investment Management. She is responsible for economic research and analysis across all regions and sectors. Bitel distills macroeconomic and geopolitical developments into actionable insights for global equity portfolios within a multifaceted strategic framework. Before joining William Blair in 2009, Olga was a senior economist at the National Institute of Economic and Social Research in London. Olga received a B.A. from the University of Chicago and an M.Sc. in economics from the London School of Economics and Political Science.