Infrastructure experts weigh in on institutional capital’s new digital obsession

Whether to include digital infrastructure in a pension portfolio is starting to be a regular conversation among portfolio allocators. After all, with data centres, cell towers, and fibre networks drawing billions in institutional capital, the debate has shifted from “should we invest?” to “how much, and where?”

Yet Zsolt Kohalmi believes pension plans are split on digital infrastructure. While some have made it a strategic priority, pushing to expand into data centres alongside their broader real estate and private asset allocations, others remain cautious.

“Because this is a relatively new and untested asset class − in particular, on the exit side − people have managed to enter, but there’s been relatively few exits,” explains Kohalmi, co-CEO and global head of real estate at Pictet Alternative Advisors. “And I think that there is a whole universe of pension plans that are waiting on the sidelines, given that uncertainty.”

What draws the more active plans in, he says, is the lease structure. Notably, data centres tend to carry contracts of 10 to 20 years, offering the kind of long-duration, inflation-linked income that fits the pension mandate. “That length of income is something that a lot of investors feel is very attractive,” he says.

Digital infrastructure allocations among pensions today range from zero to roughly five or six percent, depending on whether an investor houses the exposure in a real estate bucket or an infrastructure bucket and how each of those buckets is structured, notes Colin Lynch, managing director and head of private markets at TD Asset Management.

But Guillaume Morency sees digital infrastructure as a permanent feature of the asset class rather than a passing fad, noting that the link between digital growth and access to power ties it directly to renewables, which reinforces its long-term relevance.

“Any institutional infrastructure portfolio should have at least 15 to 25 percent allocation to digital. Otherwise, they’re missing on a big thematic that’s going to be there for the foreseeable future,” says Morency, vice president and head of infrastructure investments at Desjardins Global Asset Management.

Kohalmi explains that pension portfolios are being reshaped by a broad retreat from office and retail, sectors that have been hit by the digital shift they once helped finance. In many cases, plans that once had 50 to 60 percent of their real estate exposure in those traditional property types are now being pushed to bring that down meaningfully, creating a large pool of capital that has to be redeployed elsewhere. For example, a significant part of that money is moving into residential and niche living sectors like student and senior housing, but a growing share is also heading into digital infrastructure, especially data centres.

What makes data centres appealing, he suggests, is the combination of long lease terms and strong tenant quality. Investors can lock in long-duration income streams backed by major hyperscalers with substantial underlying businesses, which gives the cash flow a degree of comfort that many other sectors cannot match.

But he also argues the real issue isn’t the income during the lease term. Rather, it’s what happens afterward, as the asset class notably carries unusual technological risk, from changes in cooling systems to the possibility that a given site may no longer be fit for purpose by the time a lease rolls over. That makes terminal value and exit assumptions much harder to underwrite than in traditional real estate.

He also draws a distinction between urban edge facilities and remote hyperscale campuses. Edge data centres near major cities look more defensible because latency matters, power is scarce, and the underlying land usually has alternative value. Remote hyperscale sites built for large language model workloads are harder to judge. In those cases, the key question is whether the asset will still hold its value once the initial lease expires.

Andrew Parkes, managing director at Connor, Clark & Lunn (CC&L) Infrastructure, also agrees that the asset class draws a wide range of participants.

“What I’ve seen that’s really interesting in digital infrastructure is it’s an asset class that is very active across real estate funds, infrastructure funds, private equity funds, sovereign wealth funds,” he says, adding that his firm runs a diversified, mid-market infrastructure portfolio and treats digital as a complement to traditional holdings rather than a replacement for them.

“We really see investing in digital infrastructure as an opportunity to complement our portfolio, to diversify into an asset class that has some different drivers,” he says.

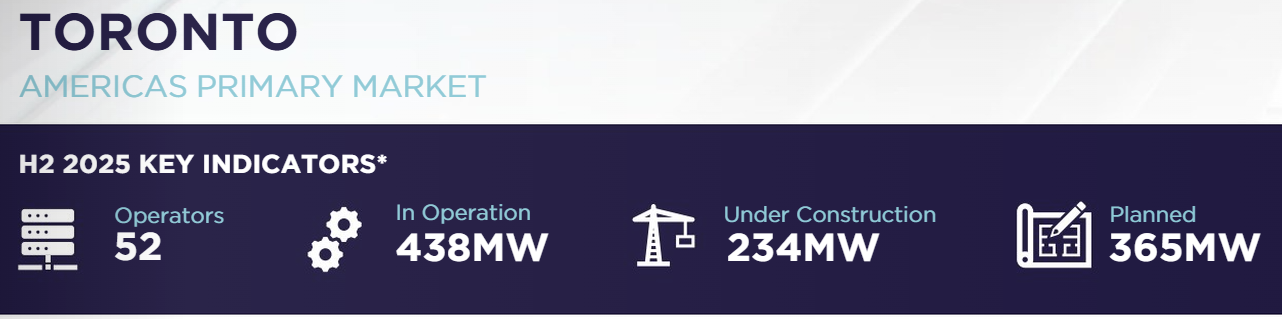

Credit: Cushman & Wakefield's Americas Data Center Update H2 2025

The appeal lies largely in the same motivation as pension funds. After all, data centres tend to carry leases of 10 to 20 years, often backed by investment-grade counterparties like Microsoft, Google, and Amazon. Those long-term cash flows, paired with fixed escalators, fit the pension mandate.

While Lynch doesn't consider digital infrastructure a core pension holding by either definition of the term, he acknowledges that could change over a 10-year horizon. Still, he argues that elevated valuations, heavy capital flows, and the dual role of hyperscalers as both customers and developers works against treating digital as a core holding today.

“That whole dynamic says the risk environment is a bit elevated today, frankly, to consider this a core holding in a pension portfolio,” he says.

For Morency, the biggest challenge in digital infrastructure is that conditions vary from one jurisdiction to the next, often in ways that aren’t obvious. He points to the contrast between rural French fibre networks, which operate under attractive regulated monopoly conditions, and the UK, where fibre has been overbuilt, causing headaches for investors.

However, the broader risk, he argues, is that “it’s easy to get rosy in digital. You get promised a lot of growth. We need to get that downside scenario locked in, because otherwise you can get burned pretty easily.”

Kaitlin Blainey, who’s also managing director at CC&L Infrastructure, frames the shift as a matter of investor maturity, noting that many pensions start with alternatives as a broad bucket and over time begin breaking it into more targeted components. She believes digital infrastructure may follow the same path that energy transition and other niche subsectors have taken, with more sophisticated allocators eventually building dedicated allocations.

Still, whether the data centre boom has gone too far and is overbuilt remains to be seen as Parkes divides the market into established and more speculative segments, noting how traditional data centres serving enterprise IT, cloud storage, and telecom networks rest on decades of proven demand, while the bigger uncertainty sits with AI-led expansion, where future use cases and improving compute efficiency make long-term needs harder to judge.

He sees the greatest risk in large training campuses built for cheap land and power rather than proximity to major economic hubs. Even so, sovereign AI and sovereign compute are driving domestic buildouts, and Canada’s capacity still trails that in the US by a wide margin, leaving room for growth, particularly in major cities with clean power.

Additionally, Kohalmi argues that data centres are far harder to model than traditional real estate because technology can change the supply-demand equation far faster than planning cycles can capture. For example, a leap in chip efficiency, new infrastructure models, or a shakeout among large language models could quickly alter how much capacity the market needs.

To that end, he suggests the sector could repeat the fibre optics buildout, where demand proved real but not every player survived. He believes edge data centres near cities remain the more defensible assets, while remote hyperscale campuses tied to AI training carry greater long-term risk, particularly for pensions and institutional investors.

“None of us quite know if we’re overbuilt or underbuilt. I think I would feel very secure in edge data centres, and I would worry slightly more around the hyperscale and large language models out in the middle of nowhere for the less defensive capabilities,” says Kohalmi.

Ultimately, while the definition of infrastructure hasn’t changed like the essential nature and physicality of the assets, the economy around it has.

“One of the core characteristics investors are focused on is the essential nature of these assets and the physicality of them. As the asset class has matured, so has the economy and our lifestyles. As a result, digital has continued to enter and grow in that conversation as we think about what is essential to our day-to-day lives and the communities in which we live and operate,” says Blainey.