Best Benefits, Pensions, and Institutional Investment Technology Providers in Canada | 5-Star Technology

Jump to winners | Jump to methodology

Circuits of trust

Canada’s technology sector is crowded, with tens of thousands of businesses competing for attention. Yet, within that volume, a small group of providers in benefits, pensions, and institutional investment are redefining how these programs are administered. They are using data, integration, and practical design to solve problems that have challenged plans and sponsors for years.

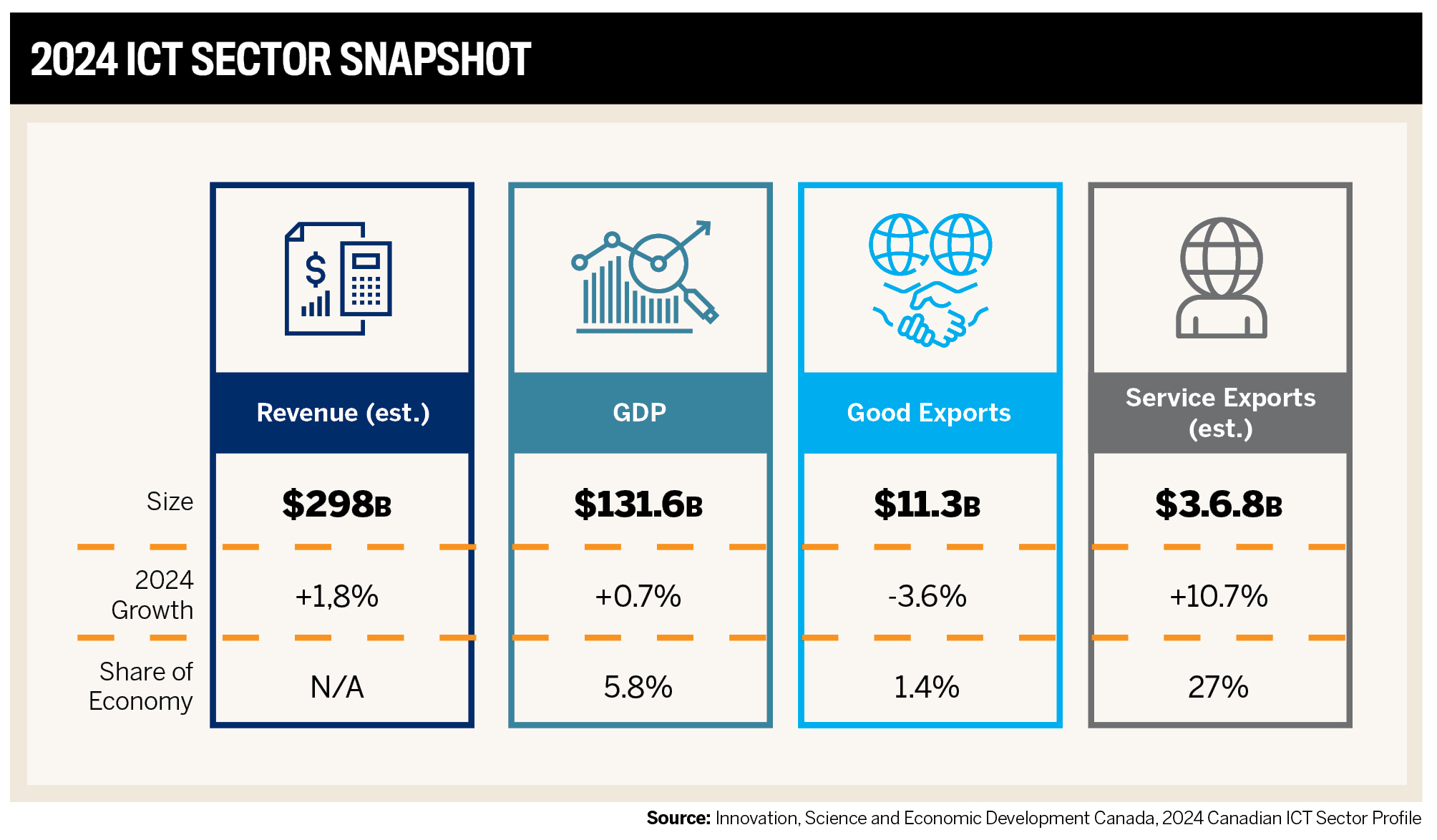

According to Innovation, Science, and Economic Development Canada’s 2024 information and communications technologies (ICT) sector profile, more than 48,000 ICT companies operate across the country. Over 44,000 of those are in software and computer services, and the majority are small:

-

approximately 41,000 employ fewer than 10 people

-

153 have more than 500 employees

While these figures reflect the full national ICT footprint, the companies highlighted in this report stood out in the benefits, pensions, and institutional investment space and were named BPM’s inaugural 5-Star Technology Providers for 2025.

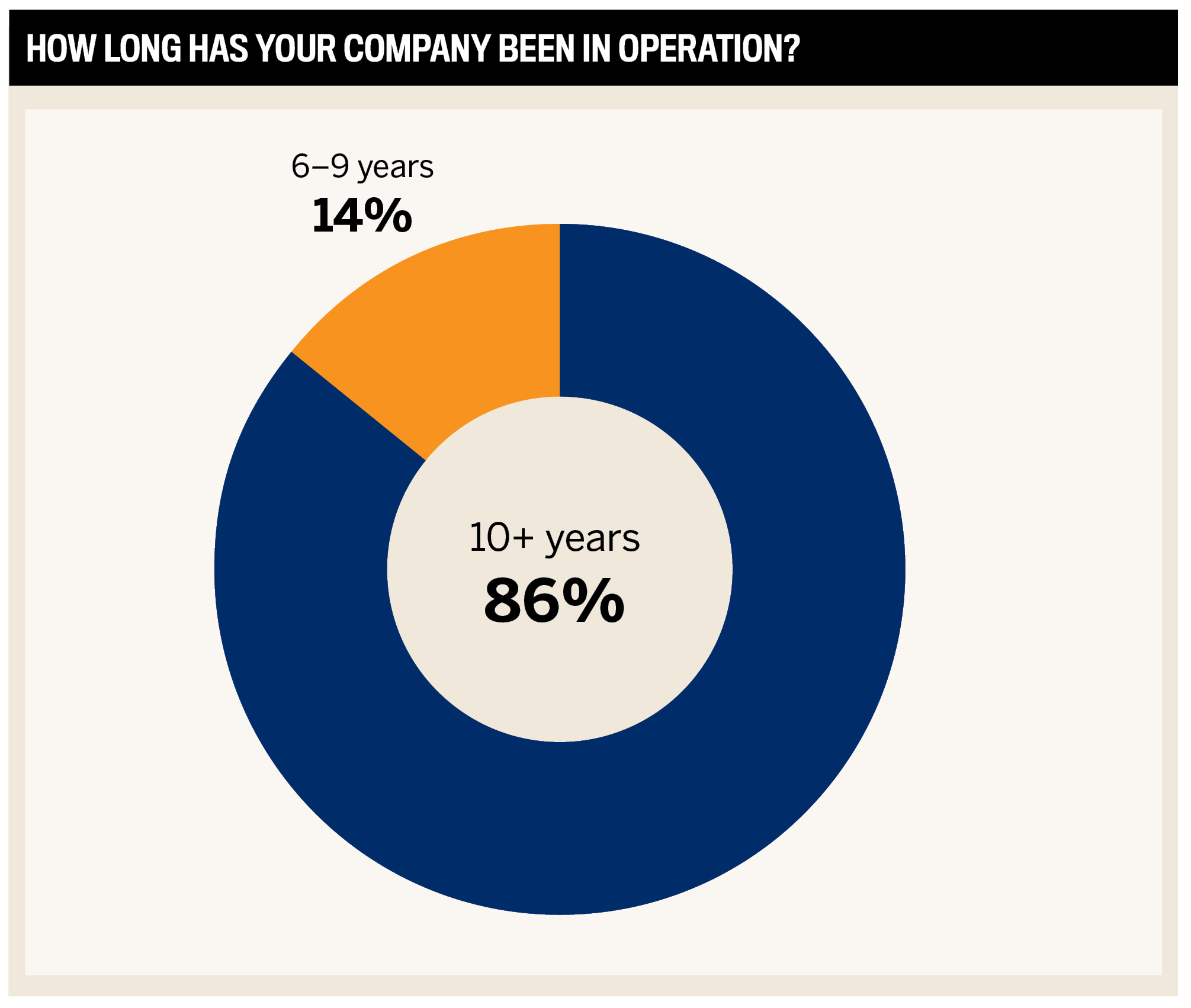

They were selected from a national pool of survey respondents, most of which have operated for more than a decade, through a structured review of their nominations that assessed the problem their technology addresses, how their solution differs from competitors, the quality of implementation and user experience, and the evidence of measurable results. Only the highest-scoring entries earned the 5-Star designation.

Industry research and BPM’s data point to three areas where the technology is most active:

-

solving data and integration problems that have become critical

-

raising the bar for member-facing experiences

-

laying the groundwork for responsible AI and analytics

Global and Canadian context for pensions and technology

Technology has become core infrastructure for Canada’s benefits, pensions, and institutional investment sector. It influences governance, member experience, and investment outcomes across plans that are better funded and more complex to administer.

Globally, pension assets rose 4.9 percent as of December 2024 to a record US$58.5 trillion, led by the largest defined contribution (DC) markets, according to a report by WTW’s Thinking Ahead Institute. DC plans now account for 59 percent of assets across the seven biggest pension markets, up from 40 percent in 2004, underscoring the migration of risk toward individuals and the intermediaries who serve them.

In Canada, demand for capital-light retirement products, rapid technology adoption, and growing allocations to alternative assets continue to influence the market.

The rise of administration platforms

Within this context, pension administration software has become a defined market segment. Across the US, the UK, and Canada, Verified Market Research valued the segment at about US$2.1 billion in 2024, with forecasts approaching US$4 billion by 2032 at an annual growth rate of roughly 8.6 percent.

What makes a 5-Star platform

The Association of Canadian Pension Management’s (ACPM) communications and marketing director, Ruth Morayniss, says a 5-Star solution balances sophistication with simplicity and only succeeds if it helps plan sponsors and members understand, engage, and make informed decisions with confidence.

“The best platforms are secure, interoperable, and intuitive, but above all, they make complex information accessible,” she explains. “When a tool enhances transparency and strengthens trust between providers, plan administrators, and members, that’s a true 5-Star solution.”

Why design must consider both members

and administrators

In practice, says Winnipeg Civic Employees’ Benefits Program CEO Cheldon Angus, today’s standout solutions put both the member journey and day-to-day administration at the forefront, rather than treating the front end as an afterthought.

Too many tools are still built by technical teams for technical users, functional on the back end but not intuitive for members. Leading platforms design for both groups and deliver that experience through secure, reliable, and scalable cloud-based SaaS.

As Angus notes, “IT departments and pension administrations are really struggling to manage the complexity of a lot of these things.” That is why demand is converging on true cloud and SaaS offerings.

Better-funded plans and risk management

Canadian defined benefit plans are entering this technology cycle in a solid financial position. The Northern Trust Canada Universe reported a 10.6 percent median return for pension plans in 2024, a result achieved despite ongoing macroeconomic volatility.

That strength carried into liability management activity. The Canadian pension risk transfer market recorded about $11 billion in group annuity transactions in 2024, according to a March 2025 Telus Health report. The volume exceeded the combined totals for 2022 and 2023 and shows how sponsors are using stronger funding levels to move risk off their balance sheets.

Stronger funding has encouraged sponsors to reduce risk exposure through annuity buy-ins and buy-outs, transfers into larger multi-employer arrangements, and more liability-aware asset mixes.

New risk management expectations

The Canadian Association of Pension Supervisory Authorities’ new risk guideline reinforces this direction. It urges administrators to adopt written frameworks that set out risk appetite, tolerance, and limits, and to ensure these guide day-to-day decision-making.

Plan sponsors are also beginning to use predictive analytics to refine actuarial assumptions and calibrate contribution schedules, even as regulators warn about data privacy and algorithmic bias risks.

As ACPM’s Morayniss observes, cybersecurity has become part of the fiduciary conversation and is reshaping how boards think about risk and the technology they are prepared to adopt.

Legacy systems meet data-driven demands

Many Canadian benefits and pension operations are still wrestling with aging, bespoke systems. A recent BPM article on 5-Star Technology winner Penad Pension Services Limited notes that numerous clients continue to rely on platforms that are no longer supported or haven’t kept pace with regulatory or technological changes, while the industry simultaneously faces an aging cohort of administrators.

What the data says

CIBC Mellon research on Canadian asset owners underscores how central data has become in this transition:

-

Nearly a quarter of pension plans (24 percent) cited data management as their top issue in managing assets internally, with another 22 percent naming it a significant secondary obstacle.

-

60 percent of plans reported significant changes in their technology and data strategies.

-

40 percent have expanded their in-house technology teams to support this shift.

However, data enrichment, tracking, and integration remain stubborn hurdles:

-

26 percent of respondents said data enrichment is the greatest obstacle to effective stakeholder reporting.

-

62 percent identified long processing times as the primary bottleneck in accessing the data needed for decisions.

-

38 percent pointed to inconsistent data as a barrier to reliable insights.

Why transformation succeeds or fails

Morayniss notes that the hardest part of adopting new technology is rarely the technology itself. “It’s the human side of change. Legacy systems, budgets, and competing priorities play a role, but success often depends on how ready leadership and governance structures are to champion transformation,” she says.

There is a need for organizations to adopt a joined-up approach.

“In a sector built on fiduciary responsibility, it’s natural to proceed carefully,” she adds. “The organizations that do this well treat technology adoption not as an IT upgrade but as a strategic shift, supported by strong governance, clear communication, and a shared understanding of purpose.”

From the implementation front lines, Angus sees the impact of this daily. Large modernization programs are now multi-year efforts across tightly integrated systems, and project burnout is real.

Too many plans, he argues, go live with “70 percent or 80 percent functionality” and face years of defect resolution because teams did not get into every detail.

Smaller organizations often struggle to validate vendor promises, underestimate the resourcing required, and try to run major implementations off the side of the desk instead of bringing in experienced support or having architectures independently audited before they build.

Founded in 1983 and based in Kitchener, ON, Penad supports public and private plans that depend on stable systems, consistent performance, and guidance drawn from the team’s experience. That combination of technology and hands-on expertise anchors Penad's role as a partner to organizations moving away from aging and fragmented tools, and is why it’s recognized on the 5-Star Technology list for 2025.

‘We’re extremely proud of our longevity, and we’ve built a good reputation. Part of that comes down to building a relationship with clients,” CEO Matthew Price explains. “We truly embed that in our culture that this is a partnership, and we get to know them and understand their business, and bring our own knowledge to assist as a springboard for consultation.”

Matthew PricePenad Pension Services Limited

What PX3000 delivers

At the heart of Penad’s offering is the PX3000 v12 solution suite, which brings core administration into one connected system that:

-

supports defined benefit and defined contribution plans

-

covers group life and health programs, social security benefits, civil service pensions, pensioner payroll, and disability management

-

handles multi-jurisdiction and multi-currency requirements

-

reflects the compliance expectations many plans face

PX3000 is structured for modular growth, and some clients begin with a core pension or benefits module and build from there. Others adopt the full suite from the outset. Real-time reporting, case management, and document management are integrated into the platform. Member and sponsor portals support the broader move toward digital self-service.

Meeting clients at the point of transition

Price highlights several patterns when clients arrive from aging or unsupported systems.

-

Legacy routines: Many teams try to replicate old processes inside PX3000 rather than use electronic document management, digital workflows, and case management tools that reduce manual work.

-

Cultural attachment: Some administrators remain tied to “the way it was,” and modernization requires questioning steps that have been in place for years. Penad addresses this issue by listening closely to frontline staff, IT teams, and administrators, and grounding each project in partnership. “These types of implementations are generally mission-critical for all of our clients, and we treat each one as such,” says Price.

-

Communication needs: Large projects can span a year or more, which introduces uncertainty. Penad focuses on regular updates, scheduled calls, and active engagement with subject matter experts on the client side to keep teams informed.

Diverse client base shaping future needs

Penad’s clients span single-employer plans to multi-employer environments across more than 15 countries. This gives Price a broad view of sector expectations, including:

-

rising demand for automation

-

richer digital interaction

-

consolidated access to pension, benefits, and other HR-related details through a single portal

Plans are moving past static portals toward more interactive, real-time tools. One direction Price highlights is the use of AI to improve information delivery to members.

“The hot topic nowadays is artificial intelligence,” he adds, noting its potential extends far beyond member explanations. AI can elevate the entire administration environment, from reducing manual effort and improving data quality to supporting compliance, forecasting, and smarter operational workflows.

Security expectations are rising as more members engage online, prompting Penad to expand multi-factor authentication, passkeys, and user education embedded directly inside the portal.

Integration also remains top of mind as clients seek technology that works seamlessly with accounting platforms, HR systems, payment processes, and investment workflows.

Demographic change is another influence. Price points to the retirement wave already underway and set to accelerate as the largest baby boomer cohort retires. This demographic shift, he says, reinforces the need for tools that deliver accessible information and enable fast, confident decision-making.

Administration informing development

Penad’s administrative practice plays an important role in the evolution of PX3000. The third-party administrators provide valuable and timely insight drawn from daily operations, helping guide enhancements and ensuring the system continues to reflect real operational needs.

“We are not just a software development firm. We have an intimate knowledge of administration,” notes Price. That experience guides product decisions, feature updates, and the overall design philosophy behind the platform.

Regular check-ins between administrative staff and developers ensure that if a feature will reduce workload or streamline a step, Penad looks for ways to build it. “If an administrator comes to us and says they need a button for xyz, we can facilitate that button.”

Continuous improvement is supported by:

-

client feedback

-

administrative insight

-

regulatory change

The result is a solution shaped by practitioners as well as technologists, and a partnership model where system design, implementation, and daily administration reinforce one another.

Cloud, workflows, and member experience

Modern administration platforms are emerging as the spine of this ecosystem. Cloud-based pension administration software is now mainstream across North America and Europe, and analysts expect cloud deployments to account for more than 70 percent of installations in the US, the UK, and Canada by 2032.

These systems bring core administration into one place by consolidating:

-

enrollment

-

benefit calculations

-

contribution tracking

-

compliance monitoring and reporting

This reduces manual work, errors, and operational risk.

Canadian case studies demonstrate the scale of change. CAAT Pension Plan’s cloud migration with DXC and ServiceNow shows how digital workflows can scale to more than 100,000 participants while reducing administrative overhead.

A new generation of cloud-native software has been designed without being held back by aging technology, putting automation, integration, and digital self-service at the centre of the proposition. Straight-through processing from digital self-service portals into core benefit engines is becoming a realistic standard.

Enhanced portals allow employees to track their pension status, access educational content, and receive timely updates. They also provide real-time data and analytics on liabilities, funding, and member demographics to support better forecasting and planning.

Yet, as Angus points out, many vendors still have work to do on the front end. After years of investment in “robust and technical” back-end systems, some have “slapped together” member portals that offer limited self-service and dated, sluggish interfaces.

In a 5-Star world, a member should be able to log in and receive a personalized experience that recognizes whether they are a new entrant, mid-career, or late-career member, and presents the right tools accordingly.

What employers expect

On the employer side, a recent WTW survey found that almost half of multinational organizations (46 percent) are prioritizing employee-facing technology, including AI-enabled tools, to support benefits management and navigation. More than half (52 percent) now view data-driven insights as a high or top priority for improving the benefits experience.

Cost and communication challenges reinforce this focus:

-

75 percent of employers are concentrating on benefits cost management

-

79 percent are actively promoting benefits and raising awareness

Morayniss describes this as a broader move away from a one-size-fits-all model toward “meet me where I am” experiences built around customized dashboards, calculators, and more targeted communications.

Institutional investment: customization and complexity

On the investment side, Canadian asset owners are steadily raising their expectations of managers and platforms. A global study by Crisil Coalition Greenwich found that 64 percent of Canadian investors, and 65 percent globally, consider customization services important.

The study also found that half of global investors are more likely to award additional mandates to managers who excel at customization.

In domestic equities, institutional investors emphasize efficient access to liquidity and high-quality brokerage services. Ease of use, reliability, quality of technical support, and proven execution quality all rank as leading factors when selecting electronic trading platforms.

The rise of private markets

Canadian institutions also continue to push deeper into private markets. In Schroders’ annual global investor survey published in the fourth quarter of 2024, 51 percent planned to increase their private debt allocations over the following year, with similarly strong intentions in infrastructure and private equity.

This mix of complex mandates, liquidity constraints, and customization is reshaping the institutional technology stack toward more sophisticated portfolio analytics, risk and liquidity tools, and stronger data infrastructure.

Angus also points out that solutions must work not only for the very largest Maple 8 funds but for the emerging “Maple middle” of $7 billion to $20 billion plans, as well as smaller university and sector plans. These segments represent a significant share of Canadian institutional demand, but are often underserved by platforms designed for either extreme.

AI, fraud, and fiduciary governance

Canada’s prudential regulator reports that about half of federally regulated financial institutions used AI in 2023 and projects that around 70 percent will do so by 2026.

In pensions specifically, experts highlight both promise and risk. AI raises privacy and accountability concerns, yet research from the CFA Institute argues that it can improve:

-

onboarding

-

member communications

-

governance

-

investment management

-

decumulation strategies when deployed with transparency, strong oversight, and a focus on supporting human decision making

Ethical and operational concerns

Morayniss sees AI and automation already streamlining routine processes and freeing people to focus on higher-value work. The bigger opportunity, she suggests, lies in using data to anticipate member needs and deliver more proactive service. But in a sector built on long-term promises, “transparency and human oversight are essential – technology should enhance, not replace, the human connection.”

Meanwhile, Angus observes an uneven pattern of adoption across plans. Some organizations have no AI tools policies, others have put governance frameworks in place and are cautiously supportive, and a few have even built contained AI tools for staff use.

Banks may be the market leaders that automate hundreds of processes, but pension plans will naturally move at a more cautious pace. Angus also warns that AI has become a buzzword in vendor marketing, with some products merely bolting on third-party tools.

For many fiduciaries, the biggest unknown is what happens “if and when something goes wrong” – how data uploaded into these tools is stored and used, and what an AI-driven breach would mean in a context where “we’ll just pay the penalty” is not an acceptable approach to privacy risk.

Fraud trends

Benefits fraud is another front where technology cuts both ways. Anti-fraud leaders in Canada, including the Canadian Life and Health Insurance Association’s vice president of anti-fraud, Joanne Bradley, report that schemes now range from casual misconduct to sophisticated collusion, with identity and credential theft on the rise.

Global survey data published by Reinsurance Group of America suggest fraud incidence of about 3.8 percent, and AI is increasingly used both to detect suspicious patterns and to manufacture more convincing fraudulent documentation. The downstream impact lands on plan sponsors and members through plan sustainability and cost.

Unsurprisingly, analysts now cite data privacy and cybersecurity concerns as key constraints on the growth of the US/UK/Canada pension administration software market.

Experts’ advice to technology service providers

From Angus’s vantage point, the bar for future-proofed solutions includes platforms that:

-

deliver equally for members and administrators

-

operate as long-term cloud-based SaaS

-

come from vendors with genuine Canadian pension and regulatory experience rather than newcomers “out of their league”

In a market where many providers now offer steep discounts to secure their first Canadian client, Angus urges plans to probe deeply into workarounds, operating model changes, and implementation capacity. He also notes that different vendors may be better suited to large modernization budgets than to mid-market or smaller projects.

“I think there’s a lot of opportunity for vendors to have conversations with each other and understand that there’s room for market segregation,” Angus adds.

Design principles for long-term value

For Morayniss, the message to providers is to “listen before you build.” The firms that add the most value are those that understand governance, regulatory, and communication realities alongside technology.

Futureproofing, she argues, is less about chasing every new feature and more about flexibility, interoperability, and user-centric design.

“Technology can move quickly, but trust moves at a human pace,” she says. “So, education and change management have to be part of the offer.”

Conclusion

-

Canada’s benefits, pensions and institutional investment sector is still constrained by legacy systems while governance expectations keep rising.

-

Member and investor demands are changing, with higher expectations for transparency, service, and digital experiences.

-

BPM’s 5-Star Technology Providers represent the leading innovators that are modernizing administration and integrating previously fragmented systems.

-

Their platforms help hardwire compliance, support better decision-making, and improve outcomes.

Best Benefits, Pensions, and Institutional Investment Technology Providers

in Canada | 5-Star Technology

- benefitsConnect

- Charli Capital

- Eckler Ltd.

- WinTech

Insights

-

Ruth Morayniss

Ruth Morayniss

Director of Communications and Marketing

Association of Canadian Pension Management -

Cheldon Angus, MBA, ICD.D, PMP

Cheldon Angus, MBA, ICD.D, PMP

Chief Executive Officer

Winnipeg Civic Employees Benefits Program

Methodology

Benefits and Pensions Monitor invited technology service providers from around Canada to submit nominations, detailing the problems or pain points their offering is designed to solve or relieve for benefits and pensions professionals and how their solution differs from those offered by competitors.

The BPM team objectively assessed each entry for detailed information, true innovation, and proven success – along with benchmarking against the other entries – to determine the

5-Star Technology Providers.